At a time when the industry is accelerating its consolidation, Circle's decision to go public reveals a seemingly contradictory yet imaginative narrative — sustained declines in net margins juxtaposed with immense growth potential. On one hand, Circle boasts exceptional transparency, robust regulatory compliance, and stable reserve income; on the other, its profitability appears surprisingly "modest" — with a net margin of just 9.3% in 2024. This apparent "inefficiency" does not stem from a flawed business model but rather unveils a deeper growth logic: as the high-interest rate dividend gradually fades and distribution cost structures grow complex, Circle is constructing a highly scalable, compliance-first stablecoin infrastructure, strategically "reinvesting" profits into market share expansion and regulatory leverage. This article traces Circle's seven-year journey to IPO, dissecting its growth potential and capitalization rationale behind low net margins through the lenses of corporate governance, business structure, and profit model.

1 Seven-Year IPO Marathon: A History of Crypto Regulatory Evolution

1.1 Paradigm Shifts in Three Capitalization Attempts (2018–2025)

Circle's上市 journey serves as a living specimen of the dynamic interplay between crypto enterprises and regulatory frameworks. Its first IPO attempt in 2018 coincided with a period of ambiguity in the U.S. Securities and Exchange Commission's (SEC) classification of cryptocurrency attributes. At the time, Circle adopted a "payments + trading" dual-engine strategy through the acquisition of the Poloniex exchange, securing $110 million in funding from Bitmain, IDG Capital, Breyer Capital, and others. However, regulatory scrutiny over the exchange business's compliance, coupled with a sudden bear market, saw its valuation plummet 75% from $3 billion to $750 million, exposing the fragility of early crypto business models.

The 2021 SPAC attempt reflected the limitations of regulatory arbitrage thinking. While merging with Concord Acquisition Corp offered a way to bypass traditional IPO scrutiny, the SEC's inquiry into stablecoin accounting practices struck at the core — demanding Circle prove USDC should not be classified as a security. This regulatory hurdle derailed the deal but inadvertently catalyzed a pivotal transformation: Circle divested non-core assets (e.g., selling Poloniex to an investment group for $150 million) and cemented its "stablecoin-as-a-service" strategic focus. From that moment onward, Circle fully committed to building USDC's compliance framework and actively pursued regulatory licenses across multiple jurisdictions globally.

The 2025 IPO choice marks the maturation of crypto firms' capitalization pathways. Listing on the NYSE requires compliance with Regulation S-K's full disclosure mandates and internal control audits under the Sarbanes-Oxley Act. Notably, the S-1 filing disclosed its reserve management mechanism in unprecedented detail: of approximately $32 billion in assets, 85% is allocated to overnight reverse repurchase agreements via BlackRock's Circle Reserve Fund, while 15% is held at systemically important financial institutions like Bank of New York Mellon. This transparency effectively establishes a regulatory equivalence to traditional money market funds.

1.2 Partnership with Coinbase: From Ecosystem Co-Building to Subtle Tensions

From USDC's inception, Circle and Coinbase collaborated via the Centre Consortium. At its 2018 founding, Coinbase held a 50% stake, leveraging a "tech-for-traffic" model to rapidly penetrate the market. Per Circle's 2023 IPO filing, it acquired the remaining 50% of Centre Consortium from Coinbase for $210 million in stock, renegotiating the USDC revenue-sharing agreement.

The current agreement reflects a dynamic game theory framework. According to the S-1, the two parties split USDC reserve income based on a proportional formula (with Coinbase reportedly receiving about 50% of reserve income), tied to the volume of USDC supplied by Coinbase. Public Coinbase data indicates it holds roughly 20% of USDC's total circulating supply in 2024. Securing approximately 55% of reserve income with just a 20% supply share poses latent risks for Circle: as USDC expands beyond Coinbase's ecosystem, marginal costs may rise non-linearly.

2 USDC Reserve Management, Equity, and Ownership Structure

2.1 Tiered Reserve Management

USDC's reserve management exhibits a clear "liquidity layering" characteristic:

- Cash (15%): Held at GSIBs like Bank of New York Mellon to address sudden redemptions.

- Reserve Fund (85%): Allocated via BlackRock-managed Circle Reserve Fund.

Since 2023, USDC reserves have been limited to cash balances in bank accounts and the Circle Reserve Fund, with its asset portfolio comprising U.S. Treasury securities with maturities under three months and overnight U.S. Treasury repurchase agreements. The portfolio's dollar-weighted average maturity is capped at 60 days, with a dollar-weighted average duration not exceeding 120 days.

2.2 Equity Classification and Tiered Governance

Per the S-1 filing submitted to the SEC, Circle will adopt a three-tier equity structure post-IPO:

- Class A Shares: Common stock issued during the IPO, carrying one vote per share.

- Class B Shares: Held by co-founders Jeremy Allaire and Patrick Sean Neville, with five votes per share but capped at 30% of total voting power, ensuring the founding team retains decision-making control post-listing.

- Class C Shares: Non-voting shares convertible under specific conditions, aligning governance with NYSE rules.

This structure balances public market financing with long-term strategic stability while preserving executive control over key decisions.

2.3 Executive and Institutional Ownership Distribution

The S-1 discloses that the executive team holds significant equity, alongside prominent venture capital firms and institutional investors (e.g., General Catalyst, IDG Capital, Breyer Capital, Accel, Oak Investment Partners, and Fidelity), each owning over 5% of shares, collectively holding more than 130 million shares. A $5 billion IPO valuation promises substantial returns for these stakeholders.

3 Profit Model and Revenue Breakdown

3.1 Revenue Model and Operational Metrics

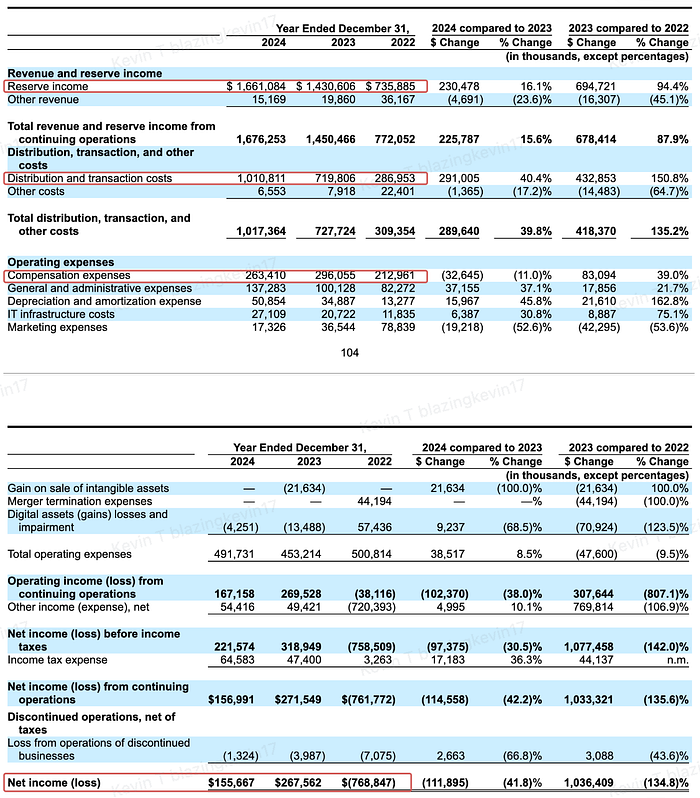

- Revenue Source: Reserve income forms Circle's core revenue stream, with each USDC token backed by an equivalent dollar amount. Invested reserve assets, primarily short-term U.S. Treasuries and repurchase agreements, generate stable interest income during high-rate cycles. S-1 data shows 2024 total revenue at $1.68 billion, with 99% ($1.661 billion) from reserve income.

- Partner Revenue Sharing: The Coinbase partnership stipulates a 50% reserve income split based on USDC holdings, reducing Circle's net income and dragging down profitability. While this split weighs on profits, it's a necessary cost for ecosystem co-building and widespread USDC adoption.

- Other Revenue: Beyond reserve interest, Circle earns from enterprise services, USDC Mint operations, and cross-chain fees, though these contribute minimally at $15.16 million.

3.2 Paradox of Revenue Growth and Profit Contraction (2022–2024)

The surface contradiction belies structural drivers:

- Convergence from Diversified to Single-Core: From 2022 to 2024, Circle's total revenue grew from $772 million to $1.676 billion, a compound annual growth rate (CAGR) of 47.5%. Reserve income now dominates, rising from 95.3% of revenue in 2022 to 99.1% in 2024. This concentration underscores the success of its "stablecoin-as-a-service" strategy but heightens reliance on macroeconomic rate fluctuations.

- Surging Distribution Costs Squeeze Gross Margins: Circle's distribution and transaction costs soared from $287 million in 2022 to $1.01 billion in 2024, a 253% increase. These costs, tied to USDC issuance, redemption, and payment settlement systems, scale rigidly with circulation growth. Unable to significantly compress these costs, Circle's gross margin dropped from 62.8% in 2022 to 39.7% in 2024, reflecting scale advantages in its B2B stablecoin model but exposing systemic profit compression risks in a rate-down cycle.

- Profitability Turns Positive but Slows Marginally: Circle achieved profitability in 2023 with a net income of $268 million and a net margin of 18.45%. In 2024, while still profitable, disposable income after operating costs and taxes fell to $101.251 million; adding $54.416 million in non-operating income yielded a net income of $155 million, but the net margin slid to 9.28%, down nearly half year-over-year.

- Cost Rigidification: Notably, 2024 general and administrative (G&A) expenses reached $137 million, up 37.1% year-over-year, marking three consecutive years of growth. Per S-1 disclosures, these costs stem from global license applications, audits, and legal/compliance team expansion, affirming the rigid cost structure of its "compliance-first" strategy.

Overall, Circle shed its "exchange narrative" in 2022, hit a profitability inflection point in 2023, and sustained profits in 2024 with decelerating growth, aligning its financial structure with traditional institutions. However, its revenue model — highly dependent on Treasury yield spreads and transaction scale — faces direct profit pressure from rate declines or USDC growth slowdowns. Sustainable profitability will require a sturdier balance between "cost reduction" and "incremental expansion."

The deeper tension lies in a business model flaw: as USDC's "cross-chain asset" attribute strengthens (2024 on-chain volume: $20 trillion), its money multiplier effect paradoxically weakens issuer profitability, mirroring traditional banking dilemmas.

3.3 Growth Potential Behind Low Net Margins

Despite net margins strained by high distribution costs and compliance spending (2024 net margin at 9.3%, down 42% year-over-year), Circle's business model and financials conceal multiple growth drivers:

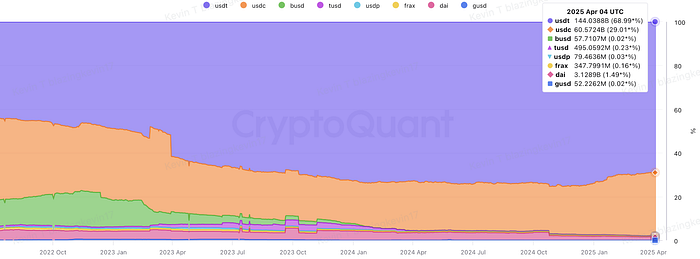

- Rising Circulation Fuels Stable Reserve Income Growth:Per CryptoQuant, as of early April 2025, USDC's market cap exceeded $60 billion, trailing USDT's $144.4 billion, with a 26% market share by late 2024 (vs. USDT). USDC's 2025 growth remains robust, adding $16 billion year-to-date. From under $1 billion in 2020, its CAGR through April 2025 reached 89.7%. Even if growth slows over the remaining eight months, a year-end market cap of $90 billion would lift CAGR to 160.5%. Though reserve income is rate-sensitive, low rates may spur USDC demand, with strong scale expansion partially offsetting downside risks.

- Structural Optimization of Distribution Costs: Despite hefty 2024 Coinbase payouts, this cost scales non-linearly with circulation. For instance, a $60.25 million one-time fee to Binance boosted its USDC supply from $1 billion to $4 billion, with per-unit acquisition costs far below Coinbase's. Per S-1, Circle's Binance partnership signals lower-cost market cap growth potential.

- Conservative Valuation Undprices Market Scarcity: Circle's $4–5 billion IPO valuation, based on $200 million adjusted net income, yields a P/E of 20–25x, aligning with PayPal (19x) and Square (22x). This reflects a "low-growth, stable-profit" market view but fails to price Circle's scarcity as the sole pure-play stablecoin stock on U.S. markets, a niche typically commanding a premium. Should stablecoin legislation pass, offshore issuers may face reserve restructuring, while Circle's compliant framework could yield a "regulatory arbitrage sunset dividend," boosting USDC market share.

- Stablecoin market capitalization shows resilience compared to Bitcoin: Stablecoin market cap remains relatively stable during significant Bitcoin price drops, highlighting its unique advantage amid crypto market volatility. In a bear market, investors often seek safe-haven assets, and the stability of stablecoin market cap growth positions Circle as a potential "safe harbor" for funds. Compared to companies like Coinbase and MicroStrategy, which heavily rely on market conditions, Circle, as the primary issuer of USDC, bases its revenue model more on stablecoin transaction volumes and interest income from reserve assets, rather than being directly impacted by crypto price fluctuations. Consequently, Circle exhibits stronger risk resistance and higher profit stability in bear markets. This makes Circle a potential hedge in investment portfolios, offering investors a protective shield, especially during intense market turbulence.

4 Risks — Stablecoin Market Upheaval

4.1 Institutional Networks No Longer an Ironclad Moat

- Double-Edged Interest Alignment: Coinbase claims 55% of reserve income despite a 20% USDC share, a legacy of the 2018 Centre agreement, effectively costing Circle $0.55 per $1 of new revenue — well above industry norms.

- Ecosystem Lock-In Risk: Binance's prepaid deal highlights channel control imbalances; if top exchanges collectively renegotiate terms, a "distribution cost spiral" could ensue.

4.2 Dual Impact of Stablecoin Legislation Progress

- Reserve Localization Pressure: Legislation mandating 100% reserves (cash and equivalents) and prioritizing U.S.-chartered custodians could impose hundreds of millions in one-time relocation costs, given Circle's current 15% cash allocation to domestic banks like Bank of New York Mellon.

5 Reflections — Strategic Window for a Trailblazer

5.1 Core Strength: Market Positioning in a Compliance Era

- Dual Compliance Network: Circle's regulatory matrix spanning the U.S., Europe, and Japan is institutional capital PayPal and others can't easily replicate. Post-Payment Stablecoin Act, its compliance cost-to-revenue ratio could drop, yielding a structural edge.

- Cross-Border Payment Substitution Wave: The "USDC instant settlement" service with Wise slashes enterprise cross-border costs. Penetrating even a fraction of SWIFT's annual volume could offset rate declines with substantial new circulation.

- B2B Financial Infrastructure: USDC's rising share in Stripe's e-commerce payments, with automated fiat conversion, cuts forex hedging costs. This "embedded finance" expansion shifts USDC from a transactional medium toward a store-of-value function.

5.2 Growth Flywheel: Interest Rate Cycles vs. Scale Economies

- Emerging Market Currency Substitution: In high-inflation regions, USDC captures portions of USD forex trades. Fed rate cuts accelerating local currency depreciation could amplify this "digital dollarization," driving circulation.

- Offshore USD Repatriation Channel: Collaborating with BlackRock on tokenized asset projects, Circle converts offshore USD deposits into on-chain assets, a "funding pipeline" value untapped in its current valuation.

- RWA Tokenization: Post-acquisition tokenized asset services have gained initial scale, with sizable annualized management fee income.

- Rate Buffer Period: With federal funds rates still elevated, Circle must accelerate internationalization to a critical circulation threshold before rate cuts are fully priced in, leveraging scale to cushion impacts.

- Regulatory Window: Pre-Payment Stablecoin Act, Circle can use its compliance edge to lock in institutional clients, signing exclusive settlement deals with top hedge funds to build exit barriers.

- Enterprise Service Suite Deepening: Packaging compliance APIs and on-chain audit tools into a "Web3 financial services cloud" for traditional banks' SaaS subscriptions opens a second non-reserve revenue stream.

Beneath Circle's low net margin facade lies a deliberate "profit-for-scale" strategy in its expansion phase. When USDC circulation exceeds $80 billion, RWA asset management scales, and cross-border payment penetration surges, its valuation logic will transform — from "stablecoin issuer" to "digital dollar infrastructure operator." This demands a 3–5-year investor lens to revalue the monopoly premium of its network effects. At the historic confluence of traditional finance and crypto economics, Circle's IPO is not just a milestone for itself but a litmus test for the industry's value reappraisal.

References:

https://www.sec.gov/Archives/edgar/data/1876042/000119312525070481/d737521ds1.htm#rom737521_10

Disclaimer: This article/blog is provided for informational purposes only. It represents the views of the author(s) and it does not represent the views of Movemaker or its affiliates. It is not intended to provide (i) investment advice or an investment recommendation; (ii) an offer or solicitation to buy, sell, or hold digital assets, or (iii) financial, accounting, legal, or tax advice. Digital asset holdings, including stablecoins and NFTs, involve a high degree of risk, can fluctuate greatly, and can even become worthless. You should carefully consider whether trading or holding digital assets is suitable for you in light of your financial condition. Please consult your legal/tax/investment professional for questions about your specific circumstances. Information (including market data and statistical information, if any) appearing in this post is for general information purposes only. While all reasonable care has been taken in preparing this data and graphs, no responsibility or liability is accepted for any errors of fact or omission expressed herein.