This week I had the opportunity again to speak truth to money, a key focus of mine. We need trillions invested the right way quickly in order to get ourselves out of the climate mess we've created. My efforts over the past 15 years to gain sufficient wisdom to create projections of what the future will look like means that organizations like Jefferies Group, now the USA's fifth-largest investment bank, engage me to speak with groups of their clients.

As with the International Energy Agency's (IEA) recent report and the Global Energy Interconnection Development & Cooperation Organization (GEIDCO), a China-created international organization created to focus on big grids, Jefferies gets that grid investment has been flat for years. Any buffer created by technical innovations like LEDs has been consumed and major generation and storage projects are waiting in long regulatory queues at present. That's part of the reason Jefferies had me give an earlier talk and Q&A on why electrification and why the grid.

This talk covered every material form of electrical generation, past and present, my rough expectation of how much of the world's energy would be provided by it in 2060 or 2080, and the implications for investments in wiring the world together.

As I reiterated in my introductory remarks, electricity is the future of all energy. It's vastly more efficient than molecules for energy and so will be much more economically viable in the future. Any pathway for energy that has to flow through created molecules like green hydrogen or synthetic fuels will be more expensive than alternatives that can electrify through batteries or grid ties. All ground transportation and all heat will be electric. And direct use of electricity has far lower negative externalities than any other option as well, so lower human health and environmental impacts too. We won't need nearly as much raw energy due to the efficiency, with perhaps 50% of the USA's current energy inputs being surplus to requirements when electricity comes mostly from wind and sun.

But that's still a lot of electricity. It's about six times what the USA generates from low-carbon forms of electrical generation today, which is a very achievable growth amount in a couple of decades. And there are very big demand centers like cities and heavy industry that won't be able to generate nearly enough electricity locally with solar to make much of a dent in demand. So building wind and solar where the wind and sun are strong and transmitting that electricity to centers of demand will be important. More transmission and beefier distribution grids are required.

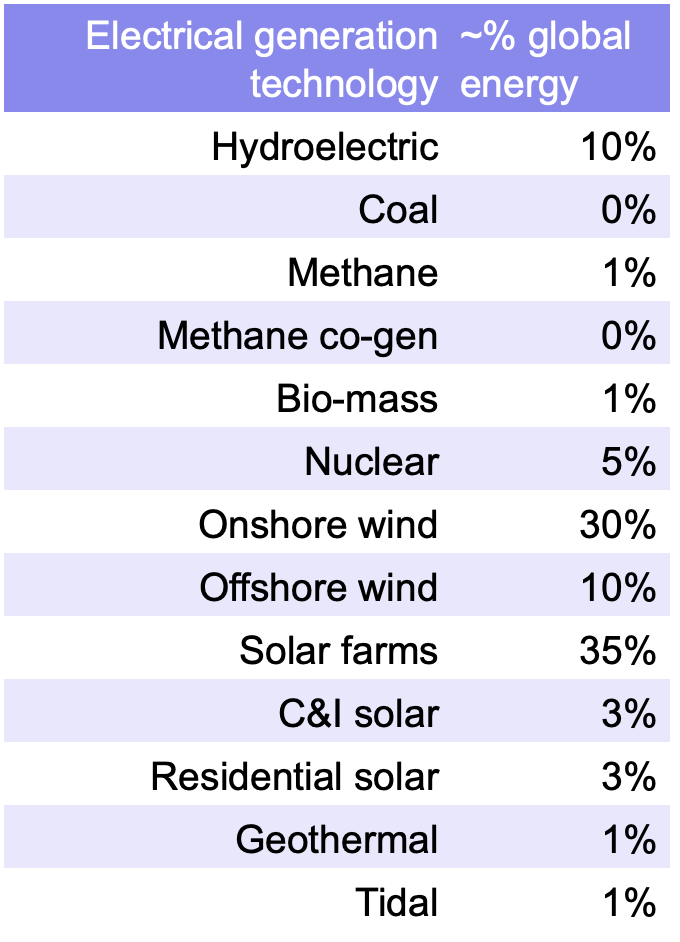

So let's start through the list of forms of generation and my outlook. The general organizing principle was legacy technologies, newer technologies that will dominate and some rounding error technologies for completeness, with some implications at the end.

As always, the error bars on multi-decadal projections are very large. This is a likely scenario based on my professional opinion, the lowest tier of the pyramid of evidence because Youtube, X, your drunk uncle and comment sections aren't even on the pyramid of evidence. Is it right? No. Is it more right than most projections? I think so.

Hydroelectric will provide ~10% of global energy

China and other geographies are still building hydroelectric and there are still large untapped resources in the north of continents. Where it's built in regions with little biomass and what biomass exists is scraped away, it pays for the carbon debt of construction relatively quickly. Hydro dams are multi-generational strategic assets. They tend to be seasonal, with higher spring generation and lower fall generation, something that often counterbalances wind generation, for example in Brasil where I looked at the patterns as part of discussions between the global tech giant I was with and Brazilian grid operators.

But they have constraints. The USA's big western dams were built during a period of unusually high precipitation, and the region has returned to being semi-arid. That aridity is being exacerbated by climate-change fueled drought and spate, leading to generation threats. China's coal generation permitting in 2022 was caused in large part by western China droughts, so their hydro fleet underperformed. That's not a permanent condition and they are building massive amounts of wind and solar, so coal will decline starting in 2024, as I pointed out recently in a piece providing nuance on the situation.

Hydroelectric's strong tendency to have synchronous generators that provide voltage and frequency control tend to make it a good fit with high-voltage alternating current (HVAC) transmission, but it can also be fitted with asynchronous generators and high voltage direct current (HVDC) transmission.

Coal generation will plummet to 0% of electrical generation

Coal remains the worst form of electrical generation for negative externalities. But like hydro and nuclear, it comes with large, spinning asynchronous turbines that have provided voltage and frequency control as a by product of their generation. That's going away and we have solutions.

Methane, aka natural gas, will drop to ~1% of global demand

We're going to be generating electricity from methane, initially as fossil natural gas and then later biomethane, somewhere for a long time. It's a convenient, cheap, high energy molecule, it stores well in salt caverns, and it will simply be used less and less and less. Further, more and more often it will be running on biomethane. It's going to be part of the dunkelflaute energy security strategies, and if some countries are forced to burn some methane for a couple of weeks a year every ten or 50 years, we're vastly ahead of where we are now. Methane is a much more sensible molecule to store for that than hydrogen.

Methane co-generation will disappear

Airports and oil sands facilities burn natural gas for electricity and heat for their buildings and processes. That's all going to be replaced by heat pumps for commercial facilities and 45% of industrial heat, and other electrical heating technologies for higher temperature industrial requirements. Alberta's oil sands will, of course, close up shop, so the vast amounts of natural gas they burn to create steam for steam assisted gravity drainage (SAGD) of underground deposits and processing of the sandy tar they extract will go away, along with that electrical generation for the grid.

Most of those facilities will add behind the meter solar and heat pumps of course, so electrical demands will increase but demands on the grid will change. Will there be a rounding error use of biomethane for co-generation? Yeah, probably, but it will be a rounding error.

Burning biomass for electricity and heat will be at most 1% of energy

As I discussed with Dr. Joseph Romm this week — watch for the podcast on Redefining Energy — Tech on November 8th — cutting down trees to pelletize them and ship them to Europe to burn makes no climate sense. It's not carbon neutral as the EU's current regulations assert, but an increasing climate problem. The EU and other places will figure that out. The co-generation of heat will be replaced by heat pumps as well. The romantic idea of wood fires is just that, romantic and not pragmatic, and this bad practice will mostly end.

Romm has three papers out or coming out through the Penn Center for Science, Sustainability, and the Media founded by Michael Mann and others. The offsets paper — tl'dr: voluntary offsets are unscalable, unjust, and unfixable — is out. Papers on bioenergy with and without carbon capture — tl'dr: climate problem, not climate solution — and direct air capture — tl'dr: why are we talking about this irrational idiocy! — are coming out November 8th.

Nuclear generation will provide ~5% of global energy

Nuclear is a decent technology. It just has high fiscal and schedule risks that are hard to overcome outside of very specific conditions. Successful scaled deployments in the past have been in periods where the programs are national strategic initiatives and aligned with nuclear weapons programs. They have been done in 2–3 decades so that the human resources can be trained, security-qualified, share leading practices and don't age out before the job is done. They have required a single design of a single nuclear technology dominate, and that engineering variances between sites are kept to an absolute minimum so that economies of scale can be found. And they require gigawatt scale reactors for thermal efficiency, so small modular reactors are very unlikely to succeed.

But there is a fair amount of nuclear energy in operation today, and some in construction. While China's renewables are growing exponentially, the nuclear program has been flat, averaging only three reactors a year since 2018 when the program peaked. This year only one reactor has been connected to the grid and it is not in commercial operation, so it is possible China will have no new additions for 2023.

I attribute that to China foregoing point three, a single design, for a different strategic imperative, something that was a mistake. That imperative was international sales and construction of Chinese nuclear reactors. China knew that other countries would want to build some nuclear, and so have deployed around eight different designs of different nuclear generation technologies to date. As such, they've eliminated economies of scale. They are exploring other nuclear designs too in prototyping and lab facilities so they are expanding this problem, not contracting it.

As a reminder, until the UK and USA decided China was a threat, not a partner, China was jointly building the Hinkley Site C reactor with France's EDF. No more.

Nuclear is also inflexible due to overlapping economic and technological reasons, something that means hot backup, storage and transmission are required to balance it. France's 75% of electricity demand from its nuclear fleet is better understood as 13% of Europe's electricity demand as the country is interconnected with transmission and net multi-TWh flows to and from neighboring countries.

Unlike hydro dams, nuclear facilities aren't intergenerational assets, they just last a bit longer than wind or solar farms. Their decommissioning costs and duration are coming home to roost.

If this sounds like nuclear energy and free market economics are really poor bed fellows, well, that's right, and as nuclear energy is a favored technology in a lot of right-wing circles, I'm sure there's a lot of cognitive dissonance over this.

Nuclear tends to be built closer to major demand centers and its synchronous generation characteristics mean HVAC transmission is beneficial.

I remain happy for almost every nuclear reactor that enters commercial operation, but this form of generation's characteristics won't make it a huge player, and its relative generation will decline substantially.

Onshore wind farms will provide ~30% of global energy demands

Onshore wind is cheap and easy to build at massive scales, with the largest wind farm right now being over 20 GW and rather absurd amounts of barely used land being suitable for it globally. HVDC transmission makes it very efficient to move electricity long distances with very low losses and wind generation is asynchronous, so HVDC is more suitable for big remote wind farms than HVAC more than not.

Power management technologies on wind farms that make them well managed contributors to the grid also mean that they can be used as fast response backup for minor variations and for frequency and voltage control. As more and more wind energy is on the grid, more of it will run a bit under maximum potential in order to game peak price spikes and to compete on ancillary services markets like the UK's new inertia market.

Onshore wind is a boring workhorse of electrical generation, the flexible coal plant of the modern grid. It's only problem is that it sticks up where people can see it and get annoyed.

Offshore wind farms will provide ~10% of global energy

It scales bigger than onshore wind because it's easier to move massive blades and masts from ports via ships to offshore sites than via rail and road to onshore sites and wind energy over the sea is higher and more consistent closer to the surface. We're building GW-scale wind farms offshore in 10 months these days. Offshore sites are barely tapped and are often much closer to major cities. Floating wind energy is coming on fast.

It will always be more expensive than onshore wind on average, but it comes with higher capacity factors to make up for it.

Because subsea cables are required to bring the electricity ashore, HVDC is always going to dominate the space. Pipelines filled with green hydrogen made at sea will remain fantasies of the molecules for energy crowd.

Western offshore wind energy's annus horribilis is part of a structural rebalancing of the market, with Chinese manufacturers building equivalent quality turbines for much lower prices and in very large numbers for their domestic markets. They are appearing in bids and being built globally. As a reminder, China built as much offshore wind in 2022 as the rest of the world did in the previous five years.

Utility-scale solar farms will generate ~35% of total energy

It's hard to beat solar farms. They just sit there. There are no moving parts. They can be built with semi-skilled labor for the most part. The components are massively iterated and cheap. They are easy to ship anywhere in the world using standard shipping containers so get the benefits of that modularity too.

And we have a lot of semi-arable and non-arable land around the world. HVDC means we can bring sunlight three hours east to power evening demand peaks, and bring sunlight far to the north from barely populated equatorial zones.

Like wind farms, the power management systems will enable them to service ancillary markets part of the time to maximize profits and reduce the need for other solutions.

C&I solar will contribute 2–3% of total energy

Distribution centers, airports, manufacturing buildings and industrial facilities — commercial and industrial (C&I) sites — will mostly get solar on their rooftops and nearby fields. It will be behind the meter and mostly used to reduce grid costs of electricity, although some will also be used as SAGD natural gas generation units are used today, to provide electricity to the grid as well at least part of the time.

There are a lot of flat rooftops in industrial parks and in ground transportation hubs. They'll get a lot of solar.

But while C&I solar will be able to provide all the net energy for a lot of commercial real estate and light industry, it won't be at the right times of day for all requirements. That's going to mean bigger, bi-directional grid connections as well as behind the meter storage.

Heavy industry is going to need very large amounts of electricity, and so distribution lines to big sites will be very beefy, and possibly classify as minor transmission lines in their own right.

Residential solar will contribute 2–3% of total energy

Rooftop solar set ups are tiny, but there are an awful lot of residential rooftops. A lot of them aren't well aligned with the sun, others are shaded by trees and a bunch of them are in the far north or south in cloudier regions where it just won't make sense to put solar on them. Most of them are privately owned, and a bunch of owners just won't want to bother as grid electricity will be just fine with lower hassle for them.

Multi-unit residential buildings are much more common outside of the developed countries than in Asia, India or Africa. There are more flat rooftops on multi-unit residential buildings, but a lot lower ration of roof area to people and energy demand in the buildings.

Like C&I, residential solar avoids some of the costs of beefing up the grid and reduces the need for some transmission, so it has merit. Net metering is a requirement for anything except the most die hard of off grid types, who are a rounding error of a rounding error on a pygmy gnat's thorax in any event.

I've discussed behind-the-meter solar scales with Mark Z. Jacobson in the past. His projections have C&I and residential solar delivering 15% of end state energy requirements. I think that's unlikely, but think 5% to 8% is probable. It's a question of degree, not a disagreement over the merit of the approach.

Geothermal and tidal might contribute 1% between them

These are rounding error technologies included because they approach 1% each. Geothermal leans into earthquake and volcano zones, and deep geothermal is interesting but multiplies long-tailed risks. Tidal has a bunch of other problems that make it equivalent to the old definition of a personal boat, i.e. a hole in the water into which you throw money.

Mining is an exception to being grid-tied

Remote mining sites have long enough lifespans, remote enough locations and usually sparsely inhabited surroundings that they will build their own renewables and storage, combinations of wind, water and solar that make sense for their geographies. With BHP, Rio Tinto and Fortescue all making it clear this year that battery and micro-grid tied mining equipment was the path forward, now it's just doing it.

Grid storage will be all over the place

Pumped hydro and various battery technologies will be reducing the need for more generation by time arbitraging electrical generation. Various segments will be met by specific technologies. Only very long duration storage for 10 or 100 year weather events is remotely difficult to do economically, and so it will be special strategic reserves. Also, it won't be hydrogen outside of countries that make bad decisions. There is nothing about hydrogen that makes it an obvious candidate for dunkelflaute storage except for starting with a desire to use hydrogen for energy. There are better molecules for that.

Heat pumps will change C&I and residential grid demand characteristics

Grid ties will get beefier because moving heat to and from the environment with electricity requires more electricity than burning natural gas for heat. But one unit of electricity moves 2–7 units of heat depending on season and air, ground or water source technologies. So it's not a linear increase.

Heat will be increasingly thought of like electricity with major generation from electricity more centrally and utility distribution through district heating in high-density areas dominating.

Electrical distribution grid sizing will become more interesting and nuanced with this.

HVDC, HVAC and distribution grids will all have generation attached

The combination of forms of generation means that every form of electrical wire in the grid will have generation attached in various ways, and a lot more of it will be bi-directional.

Interconnects between AC grids, countries and continents will mostly be HVDC, often subsea. Interconnects are inherently two-way, although some, such as the Xlink from Morocco to the UK, will only be shipping electricity north.

What does this all mean?

Legacy forms of electrical generation are going to diminish radically in significance. Total energy requirements are going to plummet. Renewable generation will dominate. Grids will become even more important. Storage will be everywhere.